Starcom Systems Research Report UPDATE:

Since my initial report was posted, I can confirm Miton have reduced as much as they intended to for the time being. The recent holdings RNS at 5% was indicative of this and my initial thoughts were then corroborated by information I've received privately, confirming that they've finished reducing.

Moreover, as Miton had shares at 20p, 8-10p and 4p the likelihood is that they will be unlikely to liquidate any of their current holdings until at least after 4p has been strong on the bid.

Starcom Systems Research Report

The below information isn't to be classed as financial advice and apologies for the out of order references - Blogger seems to disagree with the system I had!

Also, new information may be added to this report over time, as I add to my research.

Business Description (5):

Starcom Systems are an AIM listed company providing tracking systems for transportation, container, construction, utilities, telecoms, and pretty much anything high value items you might want to track.

They operate globally delivering bespoke solutions across eighteen countries.

Business Partners (5):

Some of the more notable partners and clients of Starcom Systems:

Partner with Porsche for dealer fitted tracking systems.

Watchlock (a joint venture owned by Swedish ABbloy - world’s largest lock manufacturer by volume).

SATO Global Solutions (Owned by SOFTBank - Japan)..

Cambridge Security Seals (global leader in tamper evident seals).

Great Brand.

Products (4):

The Watchlock: These were initially autonomous locking systems and the new Watchlock Pro is a significant improvement on version one thanks to the latest GPS and GSM technologies and a new version of the microprocessor with an extended battery life.

Both Mul-T-Lock and Starcom Systems will be actively marketing this new version during 2016 and customer feedback so far has been very positive. With a wholesale price that is 21% lower than the first version, it is hoped the Watchlock Pro will begin to contribute to overall sales in a meaningful way during 2016.

HELIOS: A family of tracking products comprising standard units marketed at under US$100/unit with monthly fees of $1-3 for the monitoring of vehicles, including motorbikes, linked to GPS telecom services. As the market for HELIOS is highly competitive, Starcom Systems accepts, in many cases, a low margin on the initial hardware order but are able to secure a high margin and recurring revenues.

A key example here is the Pinnacle contract in Kenya signed in December 2015. The client's main interest was to monitor speed in vehicles and enable a quick and real time reports. The initial orders have been placed and already delivered and paid for. Regular monthly shipments have commenced and are expected to continue during 2016 and beyond.

Last year Starcom Systems developed a new version called the Helios Hybrid with the advantage of being able to utilise cellular and satellite communications for tracking continuity across large and remote areas. This is a niche market enabling a significantly higher unit price and recurring prices than the standard models and consequently higher margins.

TETIS: These are products to both monitor and safeguard container traffic. Many other prospective customers are in discussion with Starcom Systems regarding these products which not only monitor location but also temperature, humidity and light penetration to detect the sudden opening of the container. Given the millions of containers shipped around the world Starcom Systems only need a small percentage to achieve a large profit from the industry.

Competing products exist but are more expensive and take much longer to install.

The strategic partnership with Contguard in the US, allows us to offer services including a complete monitoring service and rental services on a per trip basis.

Many large end users welcome the provision of such services which avoid upfront capital expenditure and this business model is expected to play a larger part in the future for this product range.

KYLOS: The Kylos Compact Device is a sophisticated portable GPS tracker designed to monitor and determine the location of assets and possessions as well as providing a means to keep family members and pets safe. Sales of this unit are slowly building since its launch two years ago.

SAS: All the units are sold with connection to a central user friendly tracking software platform which can be either owned and operated by the user or by a third party. Monthly fees vary according to the product that is connected to the SAS control hub and generate recurring revenues to Starcom Systems. As the sales and install base of all units increase, it is hoped that these revenues will increase too, in absolute terms and as a percentage of total revenues. Being 100% software, this product no longer requires significant R&D investment and is therefore a major contributor to profitability.

Company Financials (3):

General:

Market Cap: £3.74m

Shares in issue: 135,830,680

52 Week High: 8.38p

52 Week Low: 1.25p

30 Day Average Volume: 941,297

Bid: 2.25

Ask: 3.00

It’s worth noting that in reality the live spread is significantly tighter than this, but that recently the official spread has been widened by the market makers for seemingly no apparent reasons.

Recent Results (4):

- Revenue for the year of US$5.1m (2014: US$5.0m)

- Gross margin of 40% (2014: 50%)

- Loss for the period significantly reduced to US$1.8m (2014: US$2.8m)

- Overheads reduced by 27%

- Total assets of $6.77m (£4.67m)

“The Company is hopeful that it will return to profitability during the year ending 31 December 2016 by converting its strengthening pipeline into growing sales across the product range. In particular the gradual take up of Tetis and the new Watchlock Pro should contribute to this increase in sales, most of which we anticipate in the second half of the year.”

Director Credentials (much of this can be found on Starcom’s website):

Avraham (Avi) Hartmann (CEO):

Founder of Mobiltel Communication Services in 1996 and served as its CEO until it was bought-out by Pelephone, in 1999.

During this period he created a development and sales infrastructure which defined, developed, and marketed a GPS-based location product for vehicles, which was the first product of its kind in the country to use GPS technology.

In 2005, together with Doron Kedem and his son, Uri, he founded Starcom Systems.

Avi Engel:

Currently a private investor, company adviser and a non-executive director, Avi founded and led Pilat Media Global plc. as its CEO for twelve years until its sale for $100 million in March 2014.

Prior to that Avi was the CEO of Pilat Technologies International, also AIM listed and an HR services and software company.

With 25 years of public company experience on AIM and the TASE, Avi is deeply familiar with what it takes to strategize for long term shareholder value creation.

Avi holds B.Sc. in Industrial and Management Engineering from the Haifa Technion and an MBA from the Tel Aviv University.

Michael Rosenberg (Non-Executive Chairman):

Michael Rosenberg began his career in 1957 with the merchant bankers Samuel Montagu and Co Ltd, where he subsequently joined the board in 1972.

Left banking to co-found United Medical Enterprises Ltd, which provided management services and equipment services to hospitals internationally.

Michael became chairman of the British Healthcare Export Council (now known as A.B.H.I.) and led a number of trade missions overseas.

Michael was a shareholder and later chairman of what is now known as Numis Securities Plc from 1989 to 1999.

He has held a number of chairman and non-executive positions on the board of AIM-quoted companies, including Catalyst Media Group pl(current) and previously,Dori Media Ltd Pilat Media Global plc, Photon Kathaas Productions Ltd and Amiad Water Systems Ltd.

In 1994 Michael was awarded the OBE for services regarding trade with Hong Kong and has previously served as chairman of the DTI's committee on trade with Hong Kong and as a director of the China Britain Business Council.

Director Shareholdings:

Avraham (Avi) Hartmann: 20,711,168

Avi Engel: 498,334

Michael Rosenberg: 1,395,000

Uri Hartman: 22,111,166

Doron Kedmem: 22,111,166

Total Shares Held By Directors = 66,826,834

Total Number of Shares = 135,830,680

Directors Holding = 49.19% of the total issued shares.

These numbers can be confirmed in the 24th March 2016 RNS (2)

Institutional Shareholdings:

Notably Milton Group also hold 16,926,666 shares, representing 12.5% of the issued shares (6).

Appetite for Raising Funds:

Holding almost 50% of the company it’s not in the interest of the board members to issue shares like confetti as some AIM companies do and thus I get the impression that unless it’s totally necessary for the progression of the business then they won’t.

Moreover, at the recent AGM one attendee reportedly said how Michael Rosenberg had said that the company had enough cash to to continue with the current plans for at least the rest of 2016 and that while he couldn’t guarantee the need not to raise funds, he suggested that the only scenario he could foresee for doing so would be if they required more working capital to fill a very large order.

Recent News:

Expected News:

WatchLock April Launch Update (2)

Updates on sales of all products (4)

Progress reports on the Sato joint venture and penetration into the US market (4)

News on further joint ventures across the globe

GPS Tracking Sector Value

With the industry set to reach a value of $3.5bn in 2019 (1), only a small percentage of this market space is required to achieve a significant upside to the current market capitalisation of the company.

Fundamental Analysis:

The majority of the reasons to be bullish on Starcom Systems will stem from them simply being a manufacturer and primary distributor of what will likely become a ubiquitous product across many industry sectors.

In addition, the heavily invested board of directors will add to the market’s confidence in the company succeeding in the long term - this isn’t a business designed to rip off shareholders through continual dilution of equity!

Their strong underlying business model combined with a rapidly growing industry makes it quite likely that the recent share price momentum to the upside will continue, with the technical outlook corroborating this argument.

The major brands and companies Starcom Systems work alongside are a further testament to their prowess in business. A significant example is Sato Global Solutions, which has yearly revenues in excess of $900m and yet approached Starcom Systems as a joint partner!

Moreover the statement in the 11th March final results (4) that: “The Company is hopeful that it will return to profitability during the year ending 31 December 2016 by converting its strengthening pipeline into growing sales across the product range. In particular the gradual take up of Tetis and the new Watchlock Pro should contribute to this increase in sales, most of which we anticipate in the second half of the year.”, suggests that the company is likely running at a profit now and that the next set of results will be significantly improved from the last set.

These factors in combination with the company’s low level of director lent debt, make it a very exciting company (especially considering that the market capitalisation of the company is only £3.5m) in the near and medium terms with regards to their potential growth prospects.

The addition of US market maker and investment bank Stifel to quoting the shares has also led me to suspect that their sales and trading departments are advertising Starcom Systems shares to their private clients, or that a potential takeover bid/acquisition could be being processed by a US based company.

The multi-level architecture of Stifel in combination with how they have been mostly bidding for stock since commencing the quotation of Starcom Systems shares, certainly has led me to suspect that there are large private/institutional buyers circling around Starcom Systems - with an average daily volume of only around 900,000 shares at the moment your profitability only making markets is heavily limited as a new entrant.

Technical Outlook:

Macro Time Frame:

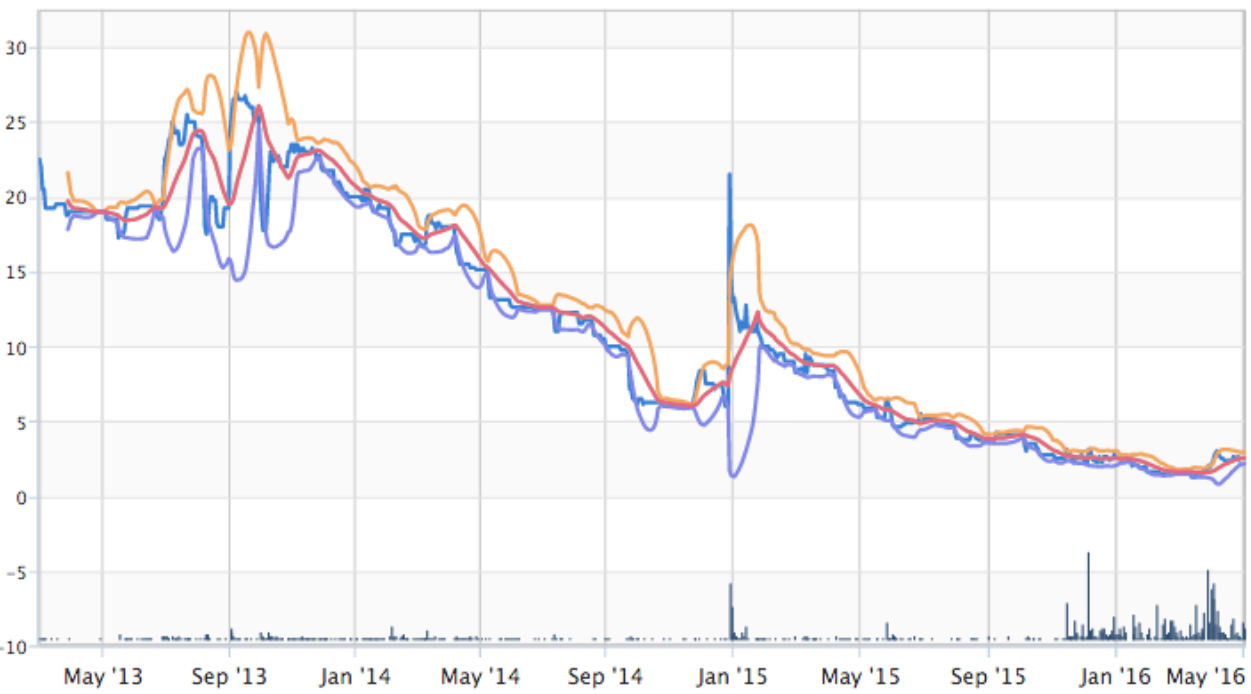

Clearly the macro time frame is a technical story of a sell down in the stock followed by a recent rally from the major lows.

This rally has coincided with a turn in some of the major moving averages, notable the 20 day moving average and its two standard deviations that make up the bollinger bands in the chart.

At these levels this is a very oversold stock from which you would expect a continuation of the trend (the backbone concept of technical analysis) in the current upwards direction.

On the sixth monthly time frame we can clearly see the reversal from the 52 week low at 1.25p and the subsequent rise to the 2-3p range.

The bollinger bands are notably beginning to tighten - often seen before an expansive upwards move in volatility - suggesting that the market is currently trading sideways awaiting new buying or selling pressure.

In particular, the previous resistance at 2.5p is now the current support level for the stock moving forwards, with support also sitting strongly at 1.6p and 1.5p.

On the three month time frame we can clearly see that a consolidation pattern is forming through a bullish pennant, which usually precedes an expansive upwards move in the new upwards trending market.

The target from a break of this pennant would be the 5p level, which conveniently sits inline with the next large resistance level.

The only real negative here is that the volume can be reasonably low, making it a possible challenge to gain liquidity in large size for some.

References:

-

-

-

-

-

http://www.lse.co.uk/share-regulatory-news.asp?shareprice=STAR&ArticleCode=9z5gqbxg&ArticleHeadline=Placing_and_Directors_Dealings