DISCLAIMER: I have no licence to distribute financial advice and thus, the following material should not be considered as such.

Central Rand Gold Ltd Research Report

Basic Information:

EPIC: CRND

Market Capitalisation: £3,610,000

Shares in Issue: 141,400,341

52 Week High: 25.13p

52 Week Low: 2.30p

Normal Market Size: 30,000 Shares

Bid (at time of writing): 2.75p

Ask (at time of writing): 2.80p

Spread: 1.82%

Central Rand Gold Limited is listed on both AIM and the JSE.

Company Description:

Central Rand Gold Limited is a gold exploration and production group assets at various stages of development in the Central Rand Goldfield on the southern outskirts of Johannesburg.

Central Rand Gold received its first New Order Mining Right from the South African Department of Mineral Resources in August 2008 and also has seven New Order prospecting rights. Altogether these rights cover an area of approximately 280 square kilometres.

The company works closely with Zhejiang Golden Machinery Plant (ZGMP) who are one of China's largest private mining machinery manufacturers. ZGMP clients rank amongst the world's largest gold and base metals producers, including ZiJin Mining, Jiangxi Copper, Zhongjin Lingnan.

ZGMP are industry leaders in crushing and grinding circuits, mixing and flotation equipment, concentration and filtration equipment and hydrometallurgy equipment.

Furthermore, ZGMP can provide ancillary goods and services to its clients including engineering services, building materials, metallurgy, nonferrous metal, electric power, chemical industry and other basic industries.

Board of Directors:

Chief Executive Officer: Lola Trollop

Interim Chairman: Mr Nathan Taylor

Recent News:

In order to avoid potential confusions, the below positive and negative points are both my personal opinions, but are taken as specific quotes from the news releases in question. The most important parts are in bold text.

Operational, Financial, Corporate & Board Update (1)

Positives:

“The Company has entered into a binding Joint Venture Tolling Agreement (the "Tolling Venture") with a third party supplier of ore for the sourcing and processing of gold-bearing material through the metallurgical plant at Central Rand Gold.”

“the Company's metallurgical plant of a minimum of 18,000 tonnes per month, commencing from July 2016. The plant currently has capacity for up to 20,000 tonnes per month and the intention of the parties in the Tolling Venture is to fully utilise that capacity.”

“the Company is presently assessing further joint venture opportunities within the region surrounding the Company's metallurgical plant. In this regard, the Company is engaging closely with its strategic partner Zhejiang Golden Machinery Plant (“ZGMP")."

“In relation to the surface joint venture opportunities currently under review, the Company is working with ZGMP to optimise the existing metallurgical plant with the objective to increase tonnage throughput and efficiencies.”

“CRG continues to identify and analyse further open pit and surface opportunities and retains the option to re-access such areas if commercially viable.”

“The Company notes that there are several private sector companies that have developed water treatment processes to extract valuable elements from the AMD for application and commercial sale to the fertilizer and construction industries. The by-product of such water treatment processes is potable water, which may be sold to industry and municipalities. The Company will continue to monitor these developments to determine if there is an opportunity for CRG to participate in the development and application of these private sector water treatment processes. The Company will continue to keep shareholders informed of any updates. The Company will ensure that background information relating to these developments is uploaded to the Company's website over the near term.”

Negatives:

“The Company has worked hard to identify and exploit various surface accessible resources over the past 18 months since the flooding of the Central Basin caused the suspension of the underground operations.”

“due to recently experienced grade variability from the surface operations, the Company has decided to cease open pit mining operations for the immediate period and will focus on rehabilitation of opened up areas, as well as processing material under the Tolling Venture. Notwithstanding this course of action, CRG continues to identify and analyse further open pit and surface opportunities and retains the option to re-access such areas if commercially viable.”

“It is also contemplated that one or more of the Joint Venture opportunities will require a capacity expansion to be conducted at CRG's metallurgical plant. The size and cost of this capacity expansion is still being considered by CRG and ZGMP. Once the necessary financial modelling and engineering design work has been completed, ZGMP has proposed that it manufacture and supply the capital goods from its facilities within China. As contemplated by the MOU signed with ZGMP in 2014, the Company can elect to pay ZGMP through the issuance of new ordinary shares in Central Rand Gold rather than in cash, subject to the required shareholder approvals and applicable rules and regulations. This option would have the benefit of reducing balance sheet strain while aligning the interests of Central Rand Gold and ZGMP.”

“As announced on 11 April 2016, the Board believes this to be the latest strategy from Puno to frustrate the operations of the Company. The Board considers the Application to be without merit and has engaged legal advisers to defend the action. Shareholders will be kept fully informed as the matter progresses.”

Bridge Funding Facility with Bergen Global (2)

Investment of up to US$4 million zero coupon convertible securities, comprising of an initial tranche of US$598,000 with the ability for up to an additional US$3.5 million to be provided by mutual consent.

In addition, the Company has today undertaken a subscription to raise US$200,000 through the subscription of 4,620,005 new ordinary shares (the "Subscription Shares) at an issue price of 3.0 pence per ordinary share (the "Issue Price") (the "Subscription"). The Subscription Shares have been conditionally subscribed for by two high net worth individuals including an existing shareholder. The investors are not related to Bergen. The Issue Price represents a premium of approximately 20% per cent. to the closing price of 2.50 pence per ordinary share on 6 June 2016.

Proceeds to be used for general working capital purposes and capital improvements to the Company's milling circuit

Expected News:

Once again, in order to avoid potential misrepresentation on my part these are quotes taken from the most recent RNS’.

“the Company is engaging closely with its strategic partner Zhejiang Golden Machinery Plant (“ZGMP”)." (1)

“Representatives from ZGMP will be onsite at CRG in early June 2016 to progress these opportunities to an investment decision stage. As soon as the Company, in consultation with ZGMP, has finalised the preferred strategy it will update Shareholders with necessary details.” (1)

“CRG continues to identify and analyse further open pit and surface opportunities and retains the option to re-access such areas if commercially viable.” (1)

“The Company will continue to monitor these developments to determine if there is an opportunity for CRG to participate in the development and application of these private sector water treatment processes. The Company will continue to keep shareholders informed of any updates. The Company will ensure that background information relating to these developments is uploaded to the Company's website over the near term.” (1)

“The Board is presently working with two parties regarding potential acquisition opportunities within Sub-Sahara Africa. Whilst discussions are at a preliminary stage, both opportunities exhibit characteristics which the Board considers appealing, namely near term cash flow potential and low capital start-up costs. The Board will continue to advance these opportunities and will advise the market as and when discussions are finalised.” (1)

“Discussions regarding the size, structure and timing of the ZGMP Investment remain ongoing but are expected to be finalised in the near term.” (1)

“The Company also eagerly awaits the judgement of the Supreme Court regarding the long running dispute with Puno relating to the shareholder funding provisions relating to the operation of Central Rand Gold SA. The Company and its Counsel remain confident of the strength of case and will keep Shareholders fully informed as the matter progresses in the Supreme Court.” (1)

“The Company will make an announcement each time any Convertible Securities are converted in whole or in part and will specify in such announcement the relevant conversion price, which will be, at Bergen's election: (a) 90% of the average of five daily volume-weighted average prices of the Shares on AIM during a specified period preceding the relevant conversion and (b) £0.0372.” (2)

Fundamental Analysis:

The latest two RNS’ from the 7th June 2016, contain many positive factors that, in my opinion, will contribute to a substantial re-rate in the share price of CRND from the current price range.

The most bullish pice of news is regarding the recent placing and the creation of the convertible securities at a significant premium to the current share price of the company. logic follows that in order for these to have been written at a significant premium, the note holders and recipients of the placed shares must believe that there is significantly bullish news to be announced and that news flow is expected to pick up in order to support the share price.

The list of expected news flow above suggests that one of the next pieces of news to come will be regarding the ZGMP investment in the capital infrastructure of the company.

Moreover, further details on the Puno court case are expected soon in combination with news on potential acquisitions within Sub-Saharan Africa.

The negative news in the above RNS’ seems to be a hangover from the flooding of their underground operation. The good news is that much of this seems to be countered by the joint Tolling venture to process at least 18,000 tonnes per month of gold ores.

Overall, the clear funding at a premium in conjunction with a variety of positive news items expected in the short term, makes Central Rand Gold Limited a highly attractive investment at the current levels.

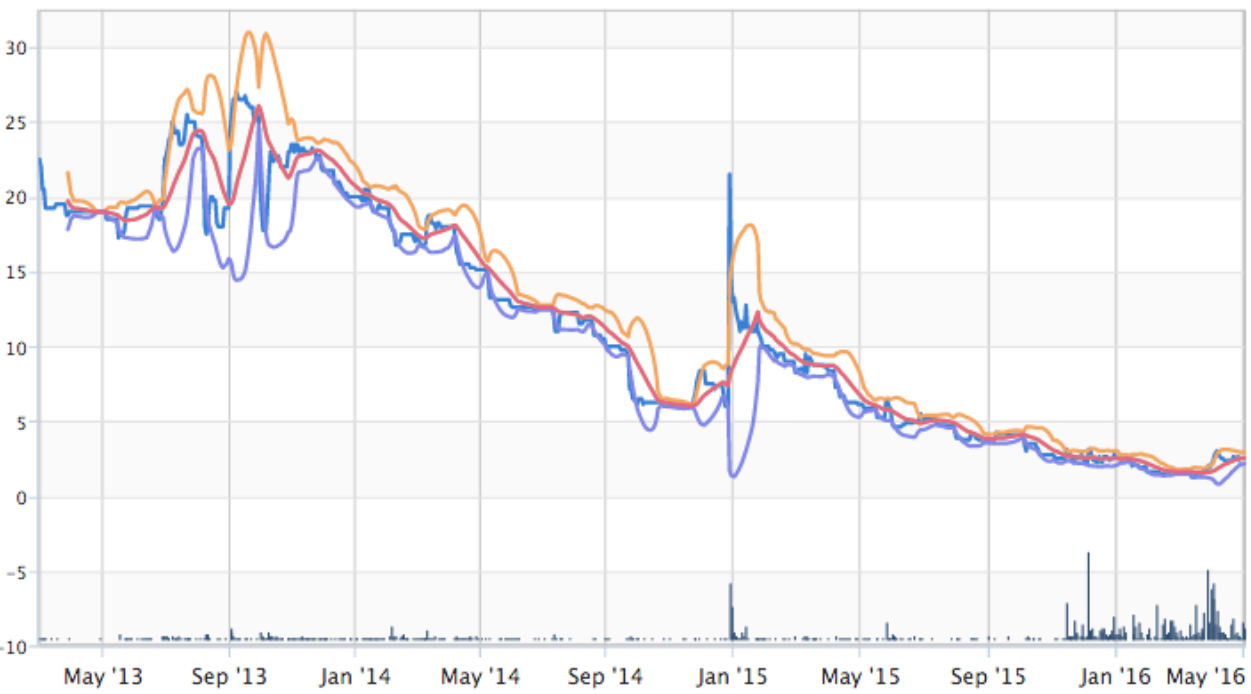

Technical Analysis:

Beginning on the longer term time frame of five years above, you can see that the company has effectively been priced to go bust for the past six-nine months. This means that a technical rebound in the region of 100-200% from the current levels is not only easily achievable, but with the surrounding of positive funding news arguably quite likely once key resistance levels at 3p have been broken. The 10p level stands out as the first key target for a medium term holder of the stock.

On the shorter time frame of six months, you can see how the expansiveness of volatility to the upside on the 7th June firmly broke the 3p resistance level, but that a short term pull back has more recently taken us back to the 2.5-2.75p spread.

Pull backs often happen around key resistance levels and invariably make it easier to break the level on the next attempt, as the price action is less impeded by trapped buyers exiting at a loss.

The high volume on this breakout of the upper Bollinger Band is especially exciting as it suggests that this isn't a false breakout as has previously happened.

The above chart is useful for showing the RSI movement through the 50 level, which in my experience is invariably a better user of the indicator than using it to judge extremes of price action. This is a firmly bullish move that suggests momentum has turned in the shorter term periods towards the upside.

References:

- http://www.lse.co.uk/share-regulatory-news.asp?shareprice=CRND&ArticleCode=yra8qt0l&ArticleHeadline=Operational_Financial_Corporate__Board_Update

- http://www.lse.co.uk/share-regulatory-news.asp?shareprice=CRND&ArticleCode=8xl0gzsk&ArticleHeadline=Bridge_Funding_Facility_with_Bergen_Global