Principally focused on the exploration and development of mineral resource deposits, Regency Mines (RGM) currently has four main projects underway: Scouting for nickel in Papua New Guinea and Kenya; copper and other minerals in Australia and agro minerals in Sudan.

Their flagship project in Papua New Guinea covers 245 potential square kilometers of nickel, with the further possibility of striking copper or gold on that same site. The company’s main interest in Australia consists of three tenements with an area of 271 square kilometers in the Fraser Range area. It also operates a mining finance and technology arm and maintains a variety of listed and non-listed holdings in the mineral resource space.

Understanding Horse Hill’s position in their portfolio:

However, if this diverse and financially compelling portfolio isn’t already good enough for you, it may be worth looking into their latest investment: a 5% direct stake in the Horse Hill Oil and Gas project.

A grouping of mining development companies are currently working together to exploit the 2,646 meter stacked oil and gas well. With an upside potential of 671 million stock barrels (“MMSTB”) of oil in place with an expected total mean recoverable prospective resources of 87 MMSTB this project seems strong. An additional 456 Bcf of natural gas (mean 164+ Bcf recoverable prospective resource) makes the project somewhat stronger. Expected to spud in late July/early August, this project is likely a great short to medium term buy, and with the further hedge of the extra mineral development projects in Regency Mine’s portfolio that are expected to spud soon (to be outlined shortly), your risk is hedged very effectively in the short term when opening a long position here.

Regency Mines would seem to be the best choice of all of the companies involved in the Horse Hill project in terms of a risk to reward basis for a number of reasons:

This particular oil field is hardly unknown, it has been explored for oil and gas for over sixty years. The producing brockham oilfield is only seven and a half kilometers away, so due to this close proximity it is highly likely that there is a significant well of oil and tests so far have been positive in outlining this too.

Regardless of the Horse Hill project exposure, the company has great future prospects as it is, due to its on going projects in Papua New Guinea and Australia, so if a spud at Horse Hill is at all disappointing (statistically unlikely), their portfolio is diverse enough that is would have little net effect to the overall company, especially remembering that this is still only viewed as a sideline project by many investors.

In other words, both the marginal indirect position Regency Mines has in the Horse Hill project, via Alba Mineral Resources (just under 0.75%), and the position it holds directly in the project (5%) are in total (just under 5.75% of the project's total exposure) self hedging through a high level of diversification in the total portfolio

Therefore the diversified resource portfolio goes a long way to remove the risk in the Horse Hill project, but the reward that Regency Mines has access to is actually magnified by the stake Regency Mines holds in Alba Mineral Resources (14.87%):

Due to Alba Mineral Resources having the lowest market capitalisation of the companies involved in the Horse Hilll project, it means that in relative terms to the other companies involved in the project, it also has the highest price volatility (and therefore market capitalisation upside) on a successful oil spud.

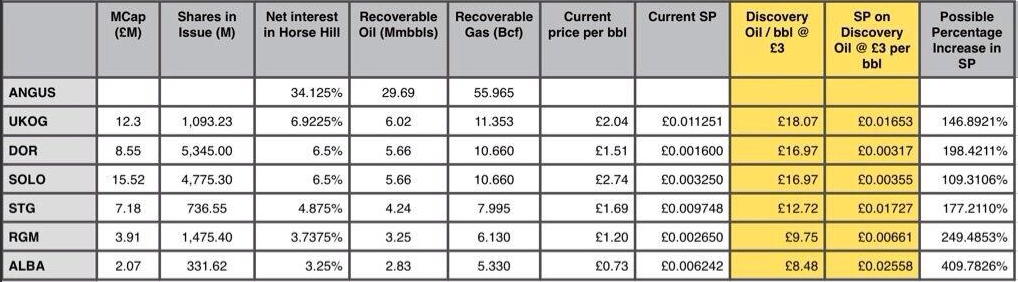

This is a point that was discussed by a professional in the oil and gas sector who posted an interesting table on his Twitter feed (https://twitter.com/ABMckinley):

While the whole table is highly interesting (albeit somewhat inaccurate now as a result of share price changes since the table’s creation), it clearly shows the high upside potential in both Regency Mines and also in Alba Mineral Resources. This means that the effective potential upside could be much more like this:

Regency Mines acquire 14.87% of the increase that Alba Mineral Resources would achieve on a successful spud (because they own 14.87% of Alba Mineral Resources), meaning that the marginal increases as a result of having an indirect stake in the project via Alba Mineral Resources yields a potential 60.96% further increase in the share price of Regency Mines on a successful spud (assuming that Alba does rise by 410%). This effectively means that in raw terms (from a share price of 0.265p - that our professional oil and gas friend on Twitter calculated), the real upside on a successful spud at Horse Hill is the sum of Regency Mines own potential percentage gain in the project with the marginal gain from Regency Mines indirect stake in Alba Mineral Resources:

249.48%+60.96% = 310.44% potential upside

Granted, there are probably significantly more sophisticated ways of doing a similar calculation, but the result that’s gained illustrates how Regency Mines has in my opinion the best upside to downside risk reward ratio.

Other Portfolio Components:

It is also engaging to note that Regency Mines further investments seem to have recently become exciting. Not long ago a report was released on the Fraser nickel drilling programme in West Africa. The main points tell us that the reconnaissance aircore drilling has ceased and the results are being processed to refine the programme's priority targets. Experts are being contracted from companies such as southern geoscience to locate possibly intrusive bodies and to pinpoint the location of nickel sulphate seams.

The project is being overseen by mining company Ram Resources (ASX:RMR), a company that Regency Mines has a 7.35% stake in. As well as this Regency Mines has a 5.6% carried interest in the Fraser project. In conclusion, Regency mines has a moderate exposure in this project, that “will generate strong news flow over the coming weeks and months, culminating in deeper drilling at what are emerging as very promising targets.” (Bill Guy, Managing Director, Ram Resources). The combination of strong newsflow and promising targets, described over the time scale of a matter of weeks will likely equate to great hype over this stock.

The other components of Regency Mines’ portfolio continue to be successful too: Red Rock Resources (LON: RRR) which is 9.80% owned by Regency Mines has recently applied (along with partner companies and contractors) for mining permits in Kenya post promising exploration for gold seams. Red Rock Resources controlling roughly 30% of possible revenue from this project, it’s inevitable that cash will flow back to Regency Mines.

Along with Red Rock Resources, Regency Mines has a 6.93% stake in Direct Nickel Limited (ASX: DIR), who have recently developed breakthrough metal ore processing technology with an unrivaled efficiency and a tiny necessary processing plant size in comparison to the current technology. Now would be a good time to remember that Regency Mines holds a large scale laterite deposit with the licences to the metals that the ore comprises. When we add two and two together we can realise that there must be a plan here utilizing the combination of the above. The best we can hope for would be a large scale mining and processing operation, with the worst case scenario being that Regency Mines finds the ore, pinpoints priority mining targets, and then sells on the land and licences to another mining company. The likelihood of failure from this opportunity is minimal because Regency Mines has the very latest technology and expertise with the partnerships to bring an opportunity like this forward. The future outlook from this network of companies is fantastic.

With the strong risk to reward ratios you can see from Regency Mines, we see this as a great opportunity for a short term trade or a medium term investment. The potential for great short term growth, with the expected long term success of the company makes this a perfect stock for a range of investor types. The newbie investors out there could grab a relatively low risk stock (for the sector) with good future promise that is still flying under the radar somewhat, while the longer term investors can take a position in a company with expected long term growth and can be reasonably sure of themselves that their money is in safe hands.

Regency Mines will only stay under the radar for so long, with the strong numbers it has the potential of generating. I’m especially impressed by the way in which the company is self-hedging with its highly diversified portfolio of investments, but moreover I feel that in the short and medium term the soon to spud Horse Hill project, showing newly calculated figures of 310.44% potential upside on a successful oil strike, could make Regency Mines a great buy in both the short and medium term.

No comments:

Post a Comment