Bacanora Minerals is an exploration-stage company focussing on borate and lithium mineral deposits in Mexico. The Company’s mineral portfolio so far includes Tubutama Borate, Magdalena Borate and Sonora Lithium projects.

I’m going to make three points in this article although I do appreciate that one could make many more in support of the company. These points are going to cover: the Resource Sector IPO curve, the relationship between Bacanora Minerals and Rare Earth Minerals and the future primary demand implications for borate and lithium globally, with special emphasis put on the Sonora Lithium project.

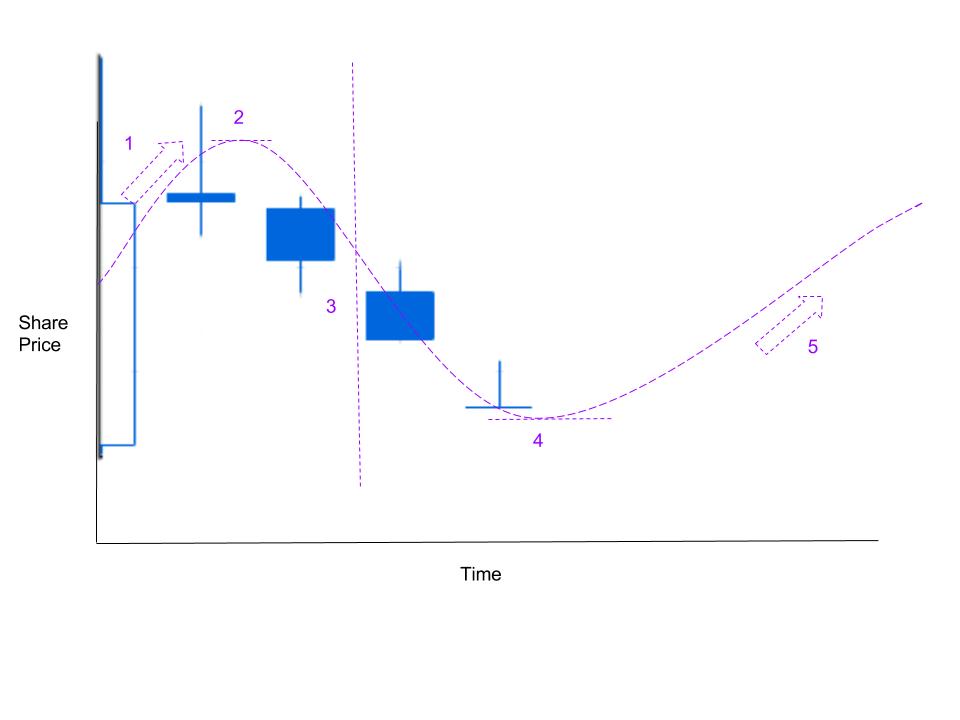

Bacanora Minerals is highly interesting for a number of reasons, which I’m going to discuss in more detail later. Primarily, I think that even without its highly positive portfolio a good trade could be made as a result of what I have christened (somewhat arrogantly) the Resource Sector IPO Curve:

Key:

1. IPO sentiment induced rise.

2. IPO sentiment reduction and IPO profit taking.

3. The stop in driven IPO sentiment and further profit taking.

4. The point of oversold.

5. The share price recovers towards IPO levels (and or above) as news-flow begins to drive the price.

Although for many this will be stating the blatantly obvious, it’s a very useful point to remember with resource sector companies, as it can greatly help making a good entry position.

Here’s what we get if we loosely overlay the daily chart since the IPO of Bacanora Minerals:

If we assume that the Resource Sector IPO Curve will hold true for Bacanora Minerals (and I see no reason to suggest that it won’t), we can see that the share price at its current levels is perfectly placed to begin the rise upwards towards £1 and beyond. Although this technique doesn’t always pan out correctly and certainly has some pitfalls, I’ve found that oftentimes it can be highly useful to ascertain when to make an entry into a resource sector stock post IPO.

Another reason why Bacanora Minerals is so interesting to me as a trader and investor is the relationship it has with another AIM listed company, Rare Earth Minerals:

Rare Earth Minerals hold an 11.94% stake in Bacanora Minerals, but they also have a 30% stake in Mexilit (with the other 70% being owned by Bacanora Minerals) under a joint venture arrangement. This effectively means that Rare Earth Minerals have a 30% stake in the El Sauz and Fleur concessions (known as the Sonora lithium project), which has been a major driver in Rare Earth Minerals’ huge share price gains this year-to-date (please see the share price following the 21st August 2013 “Final Drill Results Mexico Lithium Project” RNS for proof of this).

This relationship between the two companies is particularly useful for investors and traders, because it appears that Rare Earth Minerals is presently slightly ahead of Bacanora Minerals in terms of the share price curve (even if we ignore it’s further indirect investment in the project via its 11.94% stake in Bacanora Minerals). This relationship is most easily presented through a comparison of the two company’s market capitalisations:

Rare Earth Minerals (as of 01/08/14) =£89.71(m)

Bacanora Minerals (as of 01/08/14) =£53.61(m)

Not wanting to offend any shareholders in Rare Earth Minerals (this is after all a discussion about Bacanora Minerals) I’m going to ignore their projects in Greenland and Australia. I’m in part doing this because it avoids some maths, but also because if you were to go through the RNSs from Rare Earth Minerals and plot them on the same graph as the share price for the company, you would find that there’s a pretty strong correlation between positive news regarding the Sonora Lithium Project and the company’s share price.

If we therefore assume (yes, I appreciate that there are significant flaws to this) that both companies are valued only on their stake in the Sonora Lithium Project, we end up with a quite clear market capitalisation disparity:

Rare Earth Minerals (as of 01/08/14) = £89.71(m) for a 30% stake in the Sonora Project.

Bacanora Minerals (as of 01/08/14) = £53.61(m) for a 70% stake in the Sonora Project.

If we assume that the market is fairly valuing Rare Earth Mineral’s 30% of the Sonora Project at a share price of 1.63p and a market capitalisation £89.71(m), we would logically expect Bacanora Minerals (owning 70% of the project) to have a minimum market capitalisation of £62.79(m) or a share price of 89.06p and realistically be in a share price range between 90p and £1.10.

Furthermore, on a realistic level we have to factor in the value associated with the borate projects, with the La Ventana borate project for example going into production next year. Being 100% owned by Bacanora Minerals this is another sharp arrow to add to the quiver of profit potential and if we added the value of this project onto the current market capitalisation of Bacanora Minerals we could see a target of between £2.00-2.50.

Furthermore, on a realistic level we have to factor in the value associated with the borate projects, with the La Ventana borate project for example going into production next year. Being 100% owned by Bacanora Minerals this is another sharp arrow to add to the quiver of profit potential and if we added the value of this project onto the current market capitalisation of Bacanora Minerals we could see a target of between £2.00-2.50.

Table two entitled “Preliminary Financial Highlights”, shows quite clearly the potential value that the borate projects can add to the value of the company. The annual revenue of $25(m) on an expected mine life of twenty five years is especially exciting, as if proved it could cause a serious re-rate in the company’s share price. These borate projects added to the already misrepresented relative value of the Sonora Lithium project mean that I am personally targeting a conservatively low, but fair value around £1.50 - £2.00 with a lot of further upside potential.

Bearing in mind the above, we can now look in a more specific direction - at electric cars. Invented in the early 19th century, they saw a decline in use up until the point of 21st century technology developments and have since seen an enormous boom in use. Within the last few years the use of electric cars have more than doubled in the European Union alone (22,000 E.V.s sold in 2012 compared to the 50,000 sold in 2013) and we continue to see the growth in sales with analysts expecting electric cars to have at least 10% market dominance by 2020. The most notable recent news in this market has been automobile giant BMW Group jumping on the Electric Vehicle bandwagon with their New I3. With this we can see that the big names in the industry have realised this is a market they need a share in, and what this is going to do is push the market as well as the technology upwards as the big players try to gain dominance over the electric car.

Powered by a lithium battery, much like the one in your laptop, these cars require a good supply of raw materials. While the expected growth of the market for full electric of hybrid vehicles is still uncertain, if we follow the expected line of growth, up to 10% market share by 2020, the total number of electric cars sold in that year could be, on the low end of the guesses around 62 million or all the way up to 107 million.

So, if we take all the figures and do some maths, if 7.5 million electric cars are produced in the year 2020, with 15 kWh of batteries each containing 2 kg Li2CO3/kWh, the annual demand for the automobile industry alone would be 225,000 tons of lithium carbonate. This already a jump of 150% in demand for lithium based compounds since 2008, and we have only taken the automobile industry for the 2020 figures. Consequently the actual demand would be significantly higher still.

Take into account as well that the form of battery that the cars will need to take will likely change, that the lithium in already produced batteries isn’t easily recyclable, and that the projection figures for the growth in electric cars does not take into account the rapid urbanisation of the world, especially in LEDCs where you would expect electric cars to have dominance due to their low run cost and emissions and you have an enormous potential demand for Lithium.

If Bacanora was able to capitalise on only a small portion of this demand, the revenue streams would surely launch a company with a market cap of only £53.61(m) into a much higher status. It is only going to be so long before the big investment players take notice of this, but once they do, we can expect a bull run in the resources sector, especially those in areas related to the growing market in E.V.s such as lithium, silicon and iron.

To conclude this short piece on Bacanora Minerals, I am investing in the company on the grounds that it’s significantly undervalued at its current share price for a number of reasons. In particular the relationship between Rare Earth Minerals and the Sonora Lithium Project illustrates that there’s a long way for Bacanora Minerals to move to the upside before even that project can be viewed as fairly valued in the market place. Further to this, the increasing resource demand for Lithium in particular is a longer term indicator of potential upwards share price pressure on Bacanora Minerals, with the Resource Sector IPO Curve showing that the current share price could well be a good time to begin to move funds into the company.

No comments:

Post a Comment